How to Estimate ARV for a BRRRR Property

After-repair value, commonly called ARV, is one of the most important assumptions in a BRRRR deal.

It influences how much you can pay for the property, how much rehabilitation spending the project can support, how much equity you may create, and how much permanent financing may be available after the work is complete.

A strong ARV estimate is based on relevant closed sales, accurate property information, a defined renovation scope, and conservative adjustments. It is not simply the highest nearby sale, an online estimate, or the amount you need the property to be worth.

The objective is not to predict the appraisal perfectly. It is to develop a value range supported well enough that the project can survive a reasonable difference between your estimate and the lender’s final appraisal.

What Is ARV?

ARV is an estimate of what a property may be worth after a planned rehabilitation is completed.

For a BRRRR property, the estimate normally assumes that:

- The planned repairs have been completed

- The property is safe and functional

- Deferred maintenance has been corrected

- The finishes match the intended market

- The property can compete with renovated comparable homes

- Permits and required inspections have been completed

- The property’s legal and functional characteristics are accurately represented

ARV is therefore different from the property’s current as-is value.

A distressed property may be worth $140,000 in its current condition but have an estimated ARV of $240,000 after a substantial renovation. The $100,000 difference is not automatically profit. The project must still absorb rehabilitation, financing, holding, transaction, and refinance costs.

Where ARV Fits Into the BRRRR Process

ARV affects several stages of the complete BRRRR process.

Buy

You use ARV to determine whether the purchase price leaves enough room for repairs, financing costs, and an acceptable margin.

Rehab

The intended completed condition determines which comparable sales are relevant. Your ARV estimate and renovation plan must describe the same finished property.

Rent

ARV does not establish rent, but the property’s completed condition may affect both value and rental competitiveness.

Refinance

A lender may use the completed appraisal to determine the maximum permanent loan, subject to loan-to-value, debt-service, borrower, and program requirements.

Repeat

The amount of capital recovered at refinancing depends partly on the completed value. An overstated ARV can prevent you from recovering the amount of capital you expected to reuse.

ARV should therefore be estimated before purchase and monitored throughout the project.

ARV Is an Opinion, Not a Guaranteed Number

Even a carefully developed ARV is still an estimate.

Your eventual appraisal may differ because of:

- New sales that occur during the renovation

- Changing market conditions

- Different comparable-sale selections

- Differences in property measurements

- Differences in condition or quality ratings

- Appraiser-supported adjustments

- Unpermitted or nonconforming improvements

- A renovation that differs from the original scope

- Features you overvalued or overlooked

- Sales concessions within the comparable transactions

The Consumer Financial Protection Bureau describes an appraisal as an independent opinion of a property’s value. Your investor analysis can inform your acquisition decision, but it does not control the lender’s valuation.

The practical response is not to avoid estimating ARV. It is to estimate a range and test the project at the lower end.

The Sales Comparison Approach

For many one- to four-unit residential properties, investors estimate ARV primarily through the sales comparison approach.

You identify recently sold properties that compete with the subject property in its planned completed condition. You then analyze meaningful differences and estimate how those differences affect value.

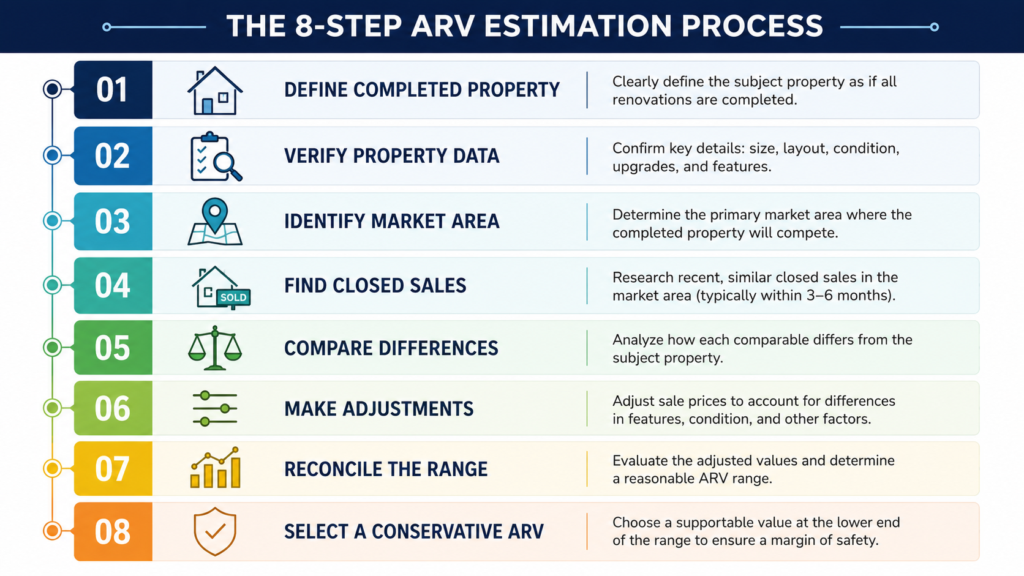

The process can be summarized as:

- Define the completed subject property.

- Collect accurate property data.

- Identify relevant closed sales.

- Verify the comparable information.

- Analyze material differences.

- Adjust the comparable sales where supportable.

- Reconcile the adjusted values into a range.

- Select a conservative working ARV.

The process is more useful than simply averaging several sale prices because nearby properties rarely have identical locations, sizes, layouts, conditions, and features.

Step 1: Define the Property in Its Completed Condition

You cannot choose good comparable sales until you define what the subject property will be after renovation.

Document the expected completed characteristics, including:

- Property type

- Above-grade living area

- Bedroom and bathroom count

- Number of units

- Architectural design

- Year built or effective age

- Basement type and finish

- Garage or parking

- Lot size

- Exterior condition

- Interior condition

- Construction quality

- Mechanical-system updates

- Functional layout

- Permitted additions

- Accessory structures

- View, traffic, or location influences

The description must reflect the actual planned project—not an idealized version of the property.

Align the ARV With the Rehab Scope

Suppose your selected comparable sales have:

- Fully updated kitchens

- Renovated bathrooms

- New roofs

- Updated electrical systems

- Modern HVAC systems

- Refinished interiors

- Strong exterior presentation

If your rehab budget includes paint, flooring, and inexpensive cabinet resurfacing but leaves major deferred maintenance unresolved, the completed subject may not compete with those sales.

The ARV and the scope of your BRRRR rehabilitation must remain aligned.

You should be able to look at each strong comparable and explain how your completed property will be similar—and where it will remain inferior.

Step 2: Confirm the Subject Property Data

An ARV estimate can fail before comparable selection if the subject property information is wrong.

Confirm important facts through several available sources, such as:

- County property records

- Tax records

- Deeds and legal descriptions

- Survey information

- MLS history

- Prior listings

- Building plans

- Permit records

- Measurements

- Inspections

- Zoning records

- Utility records where relevant

Do not rely on one listing description.

A prior listing may contain incorrect square footage, bedroom count, lot size, or renovation claims. Public records may also be incomplete or outdated.

Measure the Property Carefully

A 1,750-square-foot property and a 2,100-square-foot property may not belong in the same value range, particularly when the market reacts strongly to size.

You should also distinguish between:

- Above-grade living area

- Finished basement area

- Unfinished basement area

- Garage area

- Enclosed porches

- Converted attics

- Accessory dwelling units

- Unpermitted additions

Not every finished space is treated equally in the market or appraisal.

Verify Bedrooms and Bathrooms

Do not assume every room marketed as a bedroom will be recognized as one.

Consider:

- Egress

- Ceiling height

- Heating

- Access

- Privacy

- Local code

- Septic capacity

- Permits

- Functional layout

An unpermitted basement bedroom may contribute differently from a legal above-grade bedroom.

Step 3: Identify the Property’s Market Area

Investors often begin comparable searches with a fixed radius, such as one-half mile or one mile. That can be a useful starting point, but distance alone does not define a market.

A property across a major road may be in a different school district, municipality, tax area, development, or buyer market. A property two miles away may be more comparable if it shares the same housing stock, neighborhood characteristics, and buyer expectations.

Consider boundaries such as:

- School districts

- Major roads

- Rail lines

- Rivers

- Municipal limits

- Subdivision boundaries

- Neighborhood transitions

- Employment or commercial corridors

- Flood zones

- Property-tax districts

- Public versus private utilities

- Walkability and transportation access

The question is not merely, “How close is this sale?”

The better question is:

Would a typical buyer seriously consider both properties as alternatives?

Avoid Artificial Search Boundaries

Fannie Mae’s appraisal and property guidance does not impose a universal maximum distance for comparable sales. More distant sales may be appropriate when they are the best indicators of value and the reason for their use is explained.

That does not mean distance is irrelevant. It means market similarity matters more than an arbitrary radius.

Start close to the subject, then expand only when necessary.

Step 4: Find Relevant Closed Sales

Closed sales are normally the strongest evidence of what buyers have recently paid.

Search for properties similar to the completed subject in:

- Location

- Property type

- Design

- Living area

- Bedroom and bathroom count

- Age

- Condition

- Quality

- Lot characteristics

- Garage and parking

- Basement

- Sale date

You may begin with a broad list and then narrow it to the best three to six sales.

Closed Sales Versus Active Listings

Active and pending listings can help you understand current competition and market direction, but they do not show a completed transaction price.

An active listing shows what a seller is asking.

A pending listing may show that a buyer accepted the property at an undisclosed price.

A closed sale shows what the transaction ultimately produced, although concessions and unusual terms may still need analysis.

Use active listings as supplemental context rather than as direct substitutes for closed comparable sales.

How Recent Should Comparable Sales Be?

Recent sales are generally useful because they reflect current market conditions. However, the newest sale is not always the best comparable.

An older renovated property of the same design in the same subdivision may be more informative than a recent sale of a different property type in another market area.

Fannie Mae allows older sales when they are the most appropriate evidence, provided that market changes are analyzed and the use of the older sale is explained.

Begin with recent sales, but prioritize comparability over recency alone.

Step 5: Compare Property Type and Design

A comparable should compete with the subject property.

Avoid casually mixing:

- Detached homes and attached homes

- Single-family homes and two-unit properties

- Ranches and large multistory homes

- Manufactured homes and site-built homes

- Urban rowhouses and suburban detached homes

- Properties with acreage and standard subdivision lots

- Homes with public utilities and properties with well and septic systems

Buyers may value these property types differently even when their square footage and bedroom counts are similar.

Design Can Affect Utility

Two properties with identical living areas can have different values because one has a more functional layout.

Consider:

- Bedroom placement

- Bathroom access

- First-floor versus upper-floor living

- Walk-through bedrooms

- Low ceiling areas

- Additions with awkward access

- Laundry location

- Open versus compartmentalized layouts

- Adequate storage

- Finished area that lacks normal utility

Square footage is not a substitute for functional similarity.

Step 6: Compare Condition and Construction Quality

Condition is particularly important when estimating ARV because you are valuing the subject as though the planned work has been completed.

You should compare the subject with properties renovated to a similar standard.

A basic rental-grade renovation should not automatically be compared with a property featuring:

- Custom cabinetry

- Premium stone

- High-end appliances

- Extensive architectural upgrades

- Luxury bathrooms

- New additions

- Designer finishes

- Superior landscaping

Similarly, a fully renovated subject should not be valued primarily from dated or poorly maintained sales without appropriate analysis.

Freddie Mac explains that accurate property quality and condition ratings are important because errors can produce inappropriate comparable adjustments and unreliable value conclusions.

Renovated Does Not Always Mean Equivalent

Two listings may both use the word “renovated,” but one may have received:

- Paint

- Flooring

- New fixtures

- Resurfaced cabinets

The other may have received:

- New roof

- Updated electrical

- New plumbing

- New HVAC

- New kitchen and bathrooms

- Windows

- Insulation

- Structural repairs

Review listing histories, descriptions, photographs, permits, and available transaction information rather than relying on marketing language.

Step 7: Verify the Comparable-Sale Data

Incorrect comparable information produces unreliable adjustments.

For each serious comparable, try to verify:

- Actual sale price

- Sale date

- Property type

- Living area

- Lot size

- Bedroom and bathroom count

- Garage

- Basement

- Condition at sale

- Renovation history

- Financing terms

- Seller concessions

- Whether the transaction was arm’s length

- Whether personal property was included

- Whether the property was tenant-occupied

- Whether the sale involved unusual circumstances

The Appraisal Foundation’s guidance on collecting and verifying residential sales data emphasizes that credible sales comparison analysis depends on accurate, verified data.

Check Prior Listing Photos

Current listing photos may show the completed renovation, while prior listings can reveal the property’s previous condition.

This can help you determine:

- What work was actually completed

- Whether square footage changed

- Whether walls or rooms were reconfigured

- Whether a basement was finished

- Whether additions existed before the sale

- Whether the sale price reflects more work than your subject will receive

Photographs do not replace verified records, but they provide useful context.

Watch for Concessions

A sale at $260,000 with significant seller-paid costs may not be economically equivalent to a $260,000 sale without concessions.

You should identify known financing or seller concessions and consider whether they affected the negotiated price.

Do not automatically subtract every dollar of concessions. The relevant issue is how the market reacted to those terms.

Step 8: Remove Weak Comparables

Not every nearby renovated sale belongs in your final analysis.

Remove or reduce reliance on a property when it differs materially in ways that are difficult to measure, such as:

- Superior school district

- Waterfront or exceptional view

- Different property type

- Large acreage

- Substantially different size

- New construction

- Major accessory building

- Legal additional unit

- Superior subdivision

- Different utility system

- Unusual financing or non-arm’s-length sale

- Renovation far above the subject’s planned quality

- Location on a much better or worse street

A weak comparable does not become useful simply because it supports the value you want.

Do Not Cherry-Pick the Highest Sales

Search results may contain one unusually high sale that appears to justify the project.

Before relying on it, ask:

- Is it truly similar?

- Did it include superior land or improvements?

- Was the renovation materially better?

- Did the seller provide concessions?

- Was the sale unusual?

- Are there lower sales that are more comparable?

- Would a lender’s appraiser reasonably select it?

Your ARV should reflect the weight of the evidence, not the highest available number.

Step 9: Make Supported Adjustments

Comparable sales often require adjustments because the properties are not identical.

The basic adjustment logic is:

- If the comparable is inferior to the subject, adjust the comparable upward.

- If the comparable is superior to the subject, adjust the comparable downward.

Suppose a comparable sold for $245,000 but lacks the garage your completed property will have. If market evidence indicates that the garage contributes $10,000, the adjusted comparable value would be:

$245,000 + $10,000 = $255,000

If the comparable has a superior two-car garage and your subject has a one-car garage, the comparable may require a downward adjustment.

Common Adjustment Categories

Potential adjustments include:

- Market conditions and sale date

- Location

- View

- Lot size

- Living area

- Bedroom count

- Bathroom count

- Condition

- Construction quality

- Basement finish

- Garage or parking

- Fireplace

- Pool

- Accessory dwelling unit

- Functional layout

- Seller concessions

Not every difference requires an adjustment. The difference must have a measurable effect on how the market values the properties.

Adjustments Should Reflect Market Reaction

An adjustment should not be based solely on construction cost or a generic rule.

Fannie Mae’s guidance states that comparable adjustments should reflect the market’s reaction to differences. A universal adjustment such as a fixed amount per square foot may be inappropriate when local evidence supports a different result.

The relevant question is not:

What does this feature cost to build?

It is:

How much more or less are buyers paying for this feature in this market?

Cost Does Not Equal Contributory Value

Suppose you spend $20,000 on a premium kitchen.

That does not prove the market value increased by $20,000.

The kitchen may contribute:

- More than its cost

- Approximately its cost

- Less than its cost

- Little measurable value

The result depends on the property, neighborhood, competing inventory, renovation quality, and buyer expectations.

Why Price Per Square Foot Can Be Misleading

Price per square foot can provide a quick screening tool, but it should not be your primary ARV method.

Two properties may sell at different prices per square foot because of:

- Lot value

- Location

- Condition

- Quality

- Garage

- Basement

- Layout

- Age

- View

- Property size

- Seller concessions

- Market timing

Larger homes may also sell for a lower price per square foot because land and other fixed property components are spread over more living area.

A Quick Price-Per-Square-Foot Check

Suppose three renovated comparable sales indicate:

| Comparable | Sale price | Living area | Price per square foot |

|---|---|---|---|

| Comp 1 | $248,000 | 1,450 sq. ft. | $171 |

| Comp 2 | $260,000 | 1,550 sq. ft. | $168 |

| Comp 3 | $238,000 | 1,400 sq. ft. | $170 |

The range is approximately $168 to $171 per square foot.

Applying $169 per square foot to a 1,500-square-foot subject produces:

1,500 × $169 = $253,500

That result may be a useful reasonableness check. It does not account for garage, condition, location, lot, layout, or other differences.

Use it to identify inconsistencies—not to replace comparable-sale analysis.

Step 10: Reconcile the Comparables Into an ARV Range

After making supported adjustments, you will have several indicated values.

Do not automatically average them.

Give more weight to the comparables that are:

- Most similar

- Most recent

- Closest within the same market

- Best matched in condition

- Supported by reliable information

- Least dependent on large or uncertain adjustments

Your result should normally be a range before it becomes one working number.

For example:

- Conservative ARV: $245,000

- Probable ARV: $250,000

- Optimistic ARV: $255,000

You might use $250,000 as the working estimate but underwrite the refinance at $245,000.

ARV Example Using Three Comparable Sales

Assume your completed BRRRR property will be:

- Detached single-family home

- Three bedrooms

- Two bathrooms

- 1,500 square feet

- One-car garage

- Average subdivision lot

- Fully renovated to a solid midrange standard

You identify three renovated sales.

Comparable 1

| Item | Comparable 1 |

| Sale price | $248,000 |

| Living area | 1,450 sq. ft. |

| Bedrooms and bathrooms | 3 / 2 |

| Garage | One-car |

| Condition | Similar |

| Location | Similar |

Comparable 1 is 50 square feet smaller.

Assume supported market evidence indicates a $3,000 upward adjustment:

$248,000 + $3,000 = $251,000 adjusted value

Comparable 2

| Item | Comparable 2 |

| Sale price | $260,000 |

| Living area | 1,550 sq. ft. |

| Bedrooms and bathrooms | 3 / 2 |

| Garage | Two-car |

| Condition | Superior |

| Location | Similar |

Comparable 2 has a superior garage and somewhat better finishes.

Assume the supported adjustments are:

- Two-car versus one-car garage: −$8,000

- Superior renovation quality: −$5,000

The adjusted value is:

$260,000 − $8,000 − $5,000 = $247,000

Comparable 3

| Item | Comparable 3 |

| Sale price | $238,000 |

| Living area | 1,480 sq. ft. |

| Bedrooms and bathrooms | 3 / 2 |

| Garage | None |

| Condition | Slightly inferior |

| Location | Similar |

Assume the supported adjustments are:

- No garage: +$10,000

- Slightly inferior condition: +$4,000

The adjusted value is:

$238,000 + $10,000 + $4,000 = $252,000

Reconciled ARV

| Comparable | Sale price | Adjusted indication |

| Comparable 1 | $248,000 | $251,000 |

| Comparable 2 | $260,000 | $247,000 |

| Comparable 3 | $238,000 | $252,000 |

The adjusted range is:

$247,000 to $252,000

A reasonable working ARV may be approximately $250,000.

You might underwrite the deal using:

- $245,000 conservative value

- $250,000 probable value

- $255,000 optimistic value

The adjustment amounts in this example are illustrative. They are not standard adjustments to apply in every market.

How ARV Changes Refinance Proceeds

A relatively small ARV error can materially affect the refinance.

Assume your lender permits a 70% loan-to-value ratio.

| Appraised value | Maximum loan at 70% LTV |

| $240,000 | $168,000 |

| $245,000 | $171,500 |

| $250,000 | $175,000 |

| $255,000 | $178,500 |

| $260,000 | $182,000 |

A $10,000 change in appraised value changes the gross loan amount by:

$10,000 × 70% = $7,000

That $7,000 difference may determine whether you:

- Recover additional capital

- Leave more cash in the property

- Need to bring money to closing

- Pay off the short-term loan completely

- Qualify under the lender’s requirements

This is why appraisal risk and refinance planning should begin before you purchase the property.

You can also use the BRRRR calculator to test how different ARVs affect loan proceeds, capital remaining, and projected cash flow.

Use More Than One ARV Scenario

Do not build the project around one exact number.

Use at least three cases.

Conservative Case

Use:

- Lower end of the adjusted comparable range

- Smaller refinance

- Higher capital remaining

- No assumed appreciation during rehab

Probable Case

Use:

- Most supportable reconciled value

- Expected refinance terms

- Expected rehab outcome

Optimistic Case

Use:

- Upper end of the supportable range

- Only improvements that are actually included

- No unsupported value premiums

The deal should remain manageable in the conservative case.

If the project works only at the optimistic ARV, you are relying on the appraisal to rescue the acquisition.

How to Estimate ARV Before You Have MLS Access

MLS data can make the process more efficient, but you can begin analysis using:

- County sale records

- Public property records

- Brokerage websites

- Major real estate portals

- Local agent assistance

- Prior listings

- Auction and deed records

- Appraisal or valuation professionals

Public websites may differ in accuracy and may not disclose concessions or detailed condition information.

Use them for preliminary screening, then verify the strongest comparable sales through more reliable sources before committing capital.

Consider Working With a Local Agent

A knowledgeable agent may help you:

- Locate closed sales

- Review listing histories

- Access photographs

- Identify concessions

- Understand neighborhood boundaries

- Compare days on market

- Evaluate competing listings

- Identify sales you may have overlooked

Ask the agent to explain the evidence rather than simply provide an ARV number.

You should understand why each comparable was selected.

Can You Use an Automated Valuation Model?

An automated valuation model may provide a quick estimate based on available property and market data.

It can be useful as:

- A preliminary reference

- A reasonableness check

- A way to identify potential outliers

- A starting point for further research

It should not replace your ARV analysis.

An automated model may not understand:

- The current distressed condition

- Your planned renovation

- Interior quality

- Unpermitted space

- Functional problems

- Micro-neighborhood differences

- Recent work not reflected in records

- Differences between a cosmetic and comprehensive renovation

If an automated estimate and your comp analysis differ substantially, investigate why.

Do not simply use the higher result.

Should You Order an Appraisal Before Buying?

In some situations, you may consider obtaining an appraisal or consulting a qualified local appraiser before acquisition.

This may be useful when:

- The property is unusual

- Comparable sales are limited

- The ARV is central to a large project

- The property is in a rural market

- The renovation will materially change the property

- The project includes an accessory unit

- The property has mixed use or nonconforming characteristics

- A low valuation would create a serious liquidity problem

A pre-purchase valuation still cannot guarantee the future refinance appraisal. Market conditions, property completion, assignment requirements, and comparable sales may change.

Its purpose is to improve your analysis—not remove all valuation risk.

ARV for Small Multifamily Properties

For a duplex, triplex, or four-unit property, comparable sales may still be important, but income can become more influential.

You may need to analyze:

- Unit count

- Unit mix

- Legal use

- Current and market rent

- Operating expenses

- Utility responsibility

- Occupancy

- Property condition

- Comparable multifamily sales

- Gross rent multipliers

- Capitalization rates where relevant

A fully occupied four-unit property with documented rents may be viewed differently from a vacant property with unverified projected income.

Do not estimate a small multifamily ARV using single-family sales merely because the building looks similar from the exterior.

Special ARV Problems

Unpermitted Additions

An addition may increase usable space without receiving the same appraisal treatment as legally permitted living area.

Verify:

- Permits

- Zoning

- Construction quality

- Heating and access

- Whether the space can be legalized

- How similar properties are treated locally

Do not assume the addition will be included in above-grade living area.

Finished Basements

Finished basements can contribute value, but they may not be treated the same as above-grade space.

Compare basement characteristics such as:

- Walkout access

- Ceiling height

- Natural light

- Bathroom

- Bedroom legality

- Finish quality

- Moisture history

- Functional integration with the house

Avoid multiplying basement square footage by the above-grade price per square foot.

Accessory Dwelling Units

An accessory dwelling unit may improve utility, rent potential, and value, but its contribution depends on:

- Legality

- Permits

- Zoning

- Separate utilities

- Access

- Market acceptance

- Comparable properties with similar units

A projected rent does not automatically translate dollar-for-dollar into residential appraisal value.

Rural Properties

Rural properties may have fewer sales and greater differences in:

- Acreage

- Outbuildings

- Utilities

- Road access

- Topography

- Agricultural use

- Distance from employment

- Property type

You may need to expand the search area or use older sales, then analyze location and market changes carefully.

Rapidly Changing Markets

An older comparable may require a market-conditions adjustment when prices have changed between its sale date and the expected valuation date.

Fannie Mae requires market-condition analysis and support for time adjustments—or for the conclusion that no adjustment is necessary.

Do not assume that a six-month-old sale remains directly equivalent in a rapidly rising or declining market.

Common ARV Mistakes

Using As-Is Properties as Renovated Comparables

An as-is distressed sale may help establish current value, but it usually does not support the completed ARV directly.

Your ARV comparables should resemble the planned finished property.

Using Listings as Closed Sales

An asking price is not proof of market value.

Use listings to understand competition, not as a substitute for completed transactions.

Relying on the Highest Nearby Sale

The highest sale may have a better location, larger lot, superior renovation, additional unit, or unusual terms.

Select the most comparable sale, not the most favorable one.

Using a Universal Price-per-Square-Foot Formula

A single rate ignores location, condition, lot, garage, basement, and quality differences.

Use price per square foot only as a secondary check.

Treating Rehab Cost as Added Value

Spending $60,000 does not guarantee a $60,000 increase in value.

The market determines contributory value.

Ignoring Seller Concessions

Seller-paid costs or unusual financing can affect the economic meaning of a sale price.

Investigate the transaction when information is available.

Comparing Different Renovation Levels

A basic rental renovation should not be valued as a luxury renovation.

Your planned finish level must match the properties supporting the estimate.

Crossing Market Boundaries Without Analysis

A nearby property may belong to a different buyer market because of schools, taxes, transportation, property type, or neighborhood quality.

Explain why a sale competes with the subject.

Failing to Update the ARV

A project may take months.

Update your comparable analysis:

- Before making the offer

- Before closing

- During a long rehabilitation

- Before ordering the refinance appraisal

New sales can strengthen or weaken your original estimate.

Build an ARV Worksheet

For each serious comparable, record:

| Data point | Information to collect |

| Address | Exact property location |

| Distance and market area | Relationship to the subject |

| Sale price | Verified closed price |

| Sale date | Closing date |

| Living area | Above-grade area |

| Beds and baths | Legal and functional count |

| Property type | Detached, attached, multifamily, other |

| Year and design | Age and architectural style |

| Lot | Size and relevant characteristics |

| Garage | Type and capacity |

| Basement | Finished, unfinished, walkout, none |

| Condition | Renovation level at sale |

| Quality | Construction and finish standard |

| Concessions | Known seller or financing concessions |

| Adjustments | Supported differences |

| Adjusted value | Final indicated value |

| Reliability | High, medium, or low |

Then summarize:

- Low adjusted indication

- High adjusted indication

- Most reliable comparable

- Conservative ARV

- Probable ARV

- Optimistic ARV

- Refinance proceeds under each case

This documentation gives you a clearer basis for acquisition decisions and makes it easier to update the analysis when new sales occur.

Need to connect the ARV with the rehab budget and financing assumptions? Rehab Valuator provides advanced deal analysis, rehab estimating, comparable analysis, and investor and lender reporting when you need to evaluate the project in greater detail.

What to Provide for the Refinance Appraisal

You generally should not attempt to control the appraiser’s independent analysis. You can, however, provide accurate factual information through the lender or permitted process.

A useful property package may include:

- Completed scope of work

- Before-and-after photographs

- Permit documentation

- Final inspections

- Contractor invoices

- List of major improvements

- Dates improvements were completed

- Updated property measurements

- Lease and rent information if relevant

- Information about features that may not be obvious

- Comparable sales you believe warrant consideration

Present facts rather than demands.

A large rehabilitation budget does not prove a specific value, and an appraiser may select different comparable sales.

What if the Appraisal Is Lower Than Your ARV?

First, identify why.

Possible causes include:

- Your ARV was too aggressive

- The appraiser selected different comparables

- Your renovation quality was below the selected sales

- Market conditions changed

- Square footage or room count differed

- A property feature was not permitted

- Concessions affected your comparable sales

- The appraiser overlooked factual information

- The appraisal contains an error

Review the report for objective issues, such as:

- Incorrect living area

- Incorrect bedroom or bathroom count

- Missing garage

- Incorrect property condition

- Wrong sale information

- Inappropriate property type

- Material factual omissions

If you identify a factual or analytical concern, follow the lender’s reconsideration-of-value process.

Do not assume a lower value is wrong merely because it differs from your estimate.

Plan for the Lower Value Before Closing

Your original underwriting should explain what happens if the completed value is:

- 5% below expectations

- 10% below expectations

- Equal to total project cost

- Too low to repay short-term financing

Possible responses may include:

- Leave more capital invested

- Bring cash to the refinance

- Accept a smaller permanent loan

- Seek another appropriate lender

- Hold the property longer

- Reduce other debt

- Sell the property

- Restructure ownership or financing

The time to understand these options is before you purchase the property.

ARV Review Checklist

Before relying on your estimate, confirm that:

- You defined the completed property accurately.

- The rehab scope supports the expected condition.

- Property measurements and room counts are verified.

- Comparable sales are closed transactions.

- Comparables belong to the same buyer market.

- Property types and designs are reasonably similar.

- Renovation levels are comparable.

- Sale dates and market changes were considered.

- Concessions and unusual terms were investigated.

- Adjustments reflect market evidence rather than generic rules.

- Price per square foot is only a secondary check.

- You developed a value range rather than one unsupported number.

- Refinance proceeds were tested at the conservative value.

- The deal remains manageable if the appraisal is lower.

- The analysis will be updated before refinancing.

You can incorporate this process into a broader BRRRR deal analysis that also evaluates purchase costs, rehab risk, rent, financing, cash flow, and exit options.

Final Perspective

Estimating ARV is not a process of finding several high sales and averaging them.

You need to define the completed property, identify the correct market area, select relevant closed sales, verify the information, analyze material differences, and reconcile the evidence into a defensible range.

The most useful ARV is not the highest number you can justify.

It is the value estimate that helps you make a sound acquisition decision and prepare for a refinance that may not match your best-case projection.

When you underwrite from the lower end of a supportable range, align the renovation with the comparable properties, and test the refinance at several values, ARV becomes a risk-management tool rather than a number used to make the deal appear profitable.